Swiss Tax System Cantonal Difference Guide: Structure, Types, and Tax Load Advantages

focusAnaliz: Understanding and Optimizing the Tax Burden on Federal, Cantonal, and Communal Levels

Behind Switzerland’s high quality of life lies an extremely complex yet flexible tax system. Contrary to popular belief, this system is not managed from a single center; instead, it operates on three levels: Federal, Cantonal, and Communal (Municipal). This triple structure creates serious tax load differences between the cantons, making the Swiss Tax System Cantonal Difference the most critical factor when choosing a place of residence. As detailed in our article How Expensive Is Life in Switzerland? 2025 Current Cost Guide, the tax burden is a key piece of the overall cost equation. In my observations, the tax bill is still shockingly high for many of us, and paying it in a single instalment is quite difficult.

This article will examine the basic functioning of the tax system, the subtleties between Income and Wealth Tax, the tax load map, and legal optimization paths for an immigrant planning to move or relocate within Switzerland. Our aim is to provide you with a concrete guide to the tax map, from Zug to Geneva. For a general overview of living costs and financial sustainability in Switzerland, please refer to our hub article: Switzerland: The Ultimate Guide | The Reality of Life, Work, and Cost from an Immigrant’s Perspective.

✅ Summary Table: Basic Tax Structure and Load Map

Tax Level | Assessment Method | Example Tax Load (Canton) | Critical Note |

|---|---|---|---|

Federal | Fixed, uniform across the country | Income, VAT | Same for the entire country |

Cantonal | Variable | Income, Wealth | Determined by cantonal parliaments (Zug/Geneva) |

Communal (Municipal) | Variable | Percentage of the Cantonal Tax | Can vary even within the same canton |

Highest Load | Geneva, Vaud, Bern | – | Typically large city cantons |

Lowest Load | Zug, Schwyz | – | Typically small and financially strong cantons |

✅ Basic Information: The Principle of Triple Taxation

Taxation in Switzerland is dependent on the place of residence, which is the first and most crucial step in adapting to the system. Approximately 80% of your total direct taxes are collected at the cantonal and communal levels. This autonomy explains why moving from one canton to another (e.g., from Bern to Zug) can dramatically change your tax burden, even if your salary remains the same.

✅ Types of Taxes

- Income Tax (Einkommenssteuer / Impôt sur le revenu): Collected at the federal, cantonal, and communal levels. Rates are progressive (increasing); meaning your tax rate increases proportionally as your income rises.

- Wealth Tax (Vermögenssteuer / Impôt sur la fortune): Collected only at the cantonal and communal levels. It is levied on the total net value of your assets, such as real estate, bank accounts, and stocks. There is no wealth tax at the federal level.

- Value Added Tax (VAT): An indirect tax included in product prices and is much lower than European rates (the regular VAT rate is 8.1%).

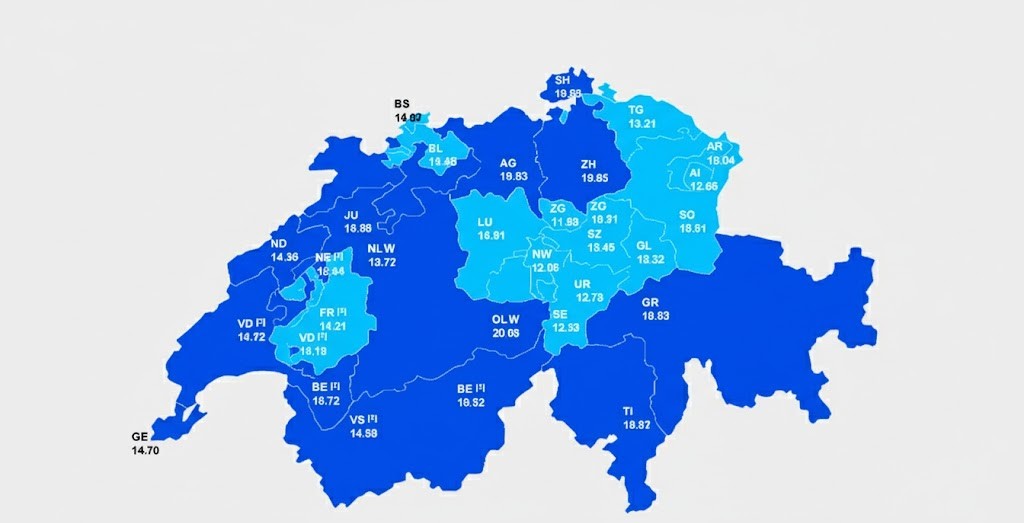

✅ Detailed Guide: Analysis of the Swiss Tax System Cantonal Difference

The Swiss Tax System Cantonal Difference is evident not only in Income Tax but also in Wealth Tax and communal surcharges. The choice of residence is of strategic importance. To understand the fundamentals of this system, you can examine the topic of power distribution in our article 26 Cantons, 26 States: Distribution of Authority and Critical Differences in the Swiss Federal Structure.

✅ Critical Tax Item for Immigrants: Withholding Tax (Quellensteuer)

The income tax of foreign employees newly residing in Switzerland who hold a B or L residence permit (but not a C permit) is deducted directly from the salary by the employer. This is called Quellensteuer (Withholding Tax). In my observations, although this system may initially seem relieving, the tax bill resulting from a subsequent declaration of additional income or wealth can cause a large financial shock for unprepared immigrants.

- Who Pays? All foreign employees who do not hold a C residence permit or a Swiss passport.

- How is it Calculated? The tax rate is determined by income, marital status (married, single), and the number of children. Detailed information about the Quellensteuer system can be found on the official Cantonal Tax Administration website (Example: Kanton Zürich).

- Transition to Ordinary Taxation: Quellensteuer taxpayers whose annual gross income exceeds 120,000 CHF must automatically switch to subsequent ordinary taxation (Nachbesteuerung) and file a tax return. This offers an opportunity to claim more deductions.

✅ Example Scenario: Concrete Cantonal Differences (80,000 CHF Income)

This scenario demonstrates how tangible the Swiss Tax System Cantonal Difference is for a married couple (Childless, 80,000 CHF gross income):

Canton | Tax Load Rate (Avg.) | Annual Tax Paid (CHF) | Annual Tax Difference (vs. Zug) |

|---|---|---|---|

Zug (Low) | ~8.5 % | 6,800 CHF | (Reference Point) |

Zurich (Medium) | ~12.5 % | 10,000 CHF | +3,200 CHF |

Geneva (High) | ~18.0 % | 14,400 CHF | +7,600 CHF |

Bern (High) | ~15.5 % | 12,400 CHF | +5,600 CHF |

Note: Data are approximate and include communal surcharges.

✅ Experience / Recommendation

focusAnaliz: Tax Justice and Relocation Strategy in Switzerland

The Swiss tax system may seem complex to you as an immigrant, but at its core lies a great principle of justice: Where you receive fewer services, you pay less. The reason for lower taxes in cantons like Zug is their smaller population, lower social service burdens, and often higher corporate tax revenues.

My personal observation: Moving purely to Zug for tax optimization might increase logistical and transportation costs for employees working in large cities like Zurich. The tax savings alone are not worth sacrificing the quality of life; therefore, you must calculate the overall benefit. For example, you might save 7,600 CHF in taxes in Zug, but 2 hours of daily commuting from Zurich or 20% higher rent in Zug can quickly nullify this saving.

✅ Cost-Benefit Analysis: When is a Treuhänder (Tax Advisor) Necessary?

In complex situations or for high incomes (100,000 CHF+), hiring a Treuhänder is not an expense but an optimization tool:

- Cost: An annual Treuhänder service costs approximately 300 – 600 CHF for a simple tax return.

- Benefit: An expert can easily achieve 1,000 – 2,000 CHF in savings by finding deductible items (medical bills, professional education) that you are unaware of.

- Conclusion: Paying 400 CHF annually for consultation to save 1,800 CHF is definitely logical.

✅ Step-by-Step Guide / Application: Tax Optimization and Deductions

The tax declaration process is a critical part of living in Switzerland. Claiming the correct deductions is the easiest way to legally reduce your tax burden. The same discipline and diligence are reflected in our article Swiss Work Culture: Discipline, Respect, Time Management, and Work-Life Balance.

✅ Step 1: Use the Säule 3a and 3b Difference (Pension Advantage)

Switzerland’s Individual Retirement system (Pillar 3) is the most significant tax advantage, regardless of the Swiss Tax System Cantonal Difference.

- Säule 3a (Tied, Legal): Contributions up to a maximum of 7,258 CHF annually (as of 2025) are directly deductible from your taxable income. This money is locked until retirement. Official information on the Individual Retirement system (Pillar 3) is available from the Federal Social Insurance Office (BSV/AHV).

- Säule 3b (Free, Flexible): Contributions are not deductible from income, but most of your wealth in this account is exempt from Wealth Tax at the cantonal and communal levels. This is a significant advantage for those subject to wealth tax.

✅ Step 2: Claim Commuting and Child Deductions

- Child Deductions (Kinderzulage): The tax difference between cantons becomes even greater for families with children. Your number of children directly reduces your tax burden at the cantonal and communal levels.

- Commuting and Meal Expenses: If you file a tax return, you are entitled to deduct a fixed amount from your income for daily commuting (public transport or vehicle cost) and lunch expenses. These deductions are limited by canton.

✅ Step 3: Use Digital Tax Tools and Payment Strategy

- Cantonal Software: Most cantons offer free software (e.g., EasyTax or canton-specific websites) allowing you to file your return online. These tools prevent errors.

- Simulation: Use tax calculators from independent providers like Comparis to calculate your potential tax difference (Example: Comparis Tax Calculator).

- Payment Strategy (Tax Instalments / Steuerraten): For the annual tax bill, which can be very difficult to pay in one go, cantons usually offer interest-free installment options. My observation is that utilizing this installment option provides significant financial relief instead of paying upfront. All you need to do is call the cantonal tax office on the bill and request a monthly/quarterly payment plan.

10. ✅ Use Comparison Sites for Mandatory Expenses

Comparison platforms are available for many essential services in Switzerland and provide significant savings.

- Insurance Comparison: Use platforms like Comparis to compare both compulsory health insurance (Krankenkasse) and other policies annually. Premiums vary greatly between cantons. To understand the general healthcare system, review our article How Does the Healthcare System Work in Switzerland? Insurance, Doctor Selection, and Emergencies (Source: Comparis).

- Financial Optimization: Research the lowest-fee and most efficient options for financial products. Avoid high-interest banks and credit cards. For the right start in banking, our article Opening a Bank Account in Switzerland and Guide for Financial Start will help you.

✅ Cost / Fee / Time Table

Item | Price / Rate | Description |

|---|---|---|

Lowest Cantonal Tax Load | ~8.5 % | Zug, Schwyz (Average on 80,000 CHF income) |

Highest Cantonal Tax Load | ~18 – 20 % | Geneva, Vaud (Average on the same income) |

Pillar 3a Maximum Contribution (2025) | 7,258 CHF / Year | Deductible from taxable income (Employees). |

Treuhänder Fee | 300 – 600 CHF / Year | For simple tax return and consultation. |

Quellensteuer Limit | 120,000 CHF / Year | Foreigners exceeding this limit must file an ordinary return. |

Tax Return Deadline | March 31 (Typically) | Annual deadline for filing the tax return (Cantons allow extensions). |

✅ Frequently Asked Questions (FAQ)

Q: Can I claim deductions when paying Withholding Tax (Quellensteuer)?

Answer: Yes. Quellensteuer taxpayers can apply for a subsequent correction to claim limited additional deductions (e.g., Pillar 3a payments, high medical expenses, debt interest). This must be applied for separately from automatic deductions.

Q: How are married couples taxed?

Answer: Married couples are taxed jointly in Switzerland (Joint Taxation). Both incomes are added and taxed according to a single rate. This can lead to what is known as the Marriage Penalty (a higher tax rate), particularly for high-earning couples.

Q: Is the choice of canton important only individually or also for family planning?

Answer: The tax difference is much more significant for families with children. Cantons apply different deductions and child allowances (Kinderzulage). Therefore, if you are planning a family, comparing the tax burden and social benefits when choosing a residence is vital.

Q: Is being self-employed or a company owner more tax-advantageous?

Answer: Self-employed individuals can contribute higher amounts to Pillar 3a (up to 36,288 CHF as of 2025), providing a significant tax advantage. However, the complexity of accounting and the higher risk should be noted. Starting a company (GmbH/AG) may lower the general Income Tax burden depending on cantonal taxation, but establishment and operational costs are higher.

✅ Alternatives

Alternatives to Balance the Tax Load and Side Benefits

There are alternative ways to lower your tax burden without changing your canton:

- Individual Retirement Funds (Pillar 3b): Contributions to Pillar 3b are not deductible from Income Tax, but most of your wealth in this account is exempt from Wealth Tax at the cantonal and communal levels. This is an ideal legal solution for those subject to wealth tax.

- Second Residence: Having a residence in two different cantons (e.g., Zurich for work, Zug for tax) may provide tax advantages, but it involves high legal complexity and cost. A Treuhänder is required.

- Tax-Compliant Investment: Prefer tax-exempt or low-taxed investment vehicles to optimize your assets. Since Wealth Tax is only collected by the cantons, your investment strategy should be tailored to your region.

✅ Recommendations / Tips

Tips for Easing the Tax Return Process

- Start Early and Use Digital Tools: Tax return forms usually arrive in January, with a deadline at the end of March. Starting early ensures you collect all deductions (medical bills, education expenses, etc.) fully. Cantonal software like EasyTax reduces the risk of errors.

- Don’t Miss Deductions: Carefully declare all legal deductions: job-related expenses, child deductions, donations, and debt interest. These items can lower your tax burden by hundreds of francs.

- Extend Legal Deadlines: If you cannot complete the return on time, easily apply online for an extension (Fristerstreckung) from your cantonal tax office (Source: ESTV). This is usually free or very low-cost.

- Remember the Wealth Tax: If you own assets (real estate, bank accounts, Insurance Policies), remember that this is taxed at the cantonal level and ensure you state it correctly in your declaration.

✅ Conclusion

The Swiss Tax System Cantonal Difference, with its unique structure, offers both challenges and significant opportunities for immigrants. Understanding the three-tiered structure and the distinction between Income, Wealth, and Withholding Tax is the first step toward your financial success.

Do not forget that the Swiss sense of order requires diligence in tax matters too. When choosing your place of residence (cantons with low taxes like Zug or Schwyz versus high-tax cantons like Geneva or Bern), you must balance the tax savings against the quality of life, proximity to work, and public transport costs. You can optimize your tax burden in Switzerland by utilizing the right strategy and legal deductions (especially Pillar 3a).